Why we get stuck in the comfort zone

Have you ever found yourself in a relationship where things weren't necessarily terrible, but weren't great either? You know, that kind of relationship that isn't ideal but isn't a complete disaster, making it difficult to end things?

Well, I've been there.

Being in that state of limbo may feel comfortable, but it's actually a highly dangerous situation.

In fact, it's the worst situation you can find yourself in because it guarantees a mediocre life.

Let me explain.

You're just getting by, if....

- your health is not terrible but you can still run after the bus

- your partner is unfulfilling but you still like them

- your job is boring but you still get benefits

- your finances are not ideal but you can still survive

It's not bad, but it's not good either.

And that's the problem—it's not bad enough to motivate you to make changes in your life.

So, you end up staying in that state, feeling somewhat comfortable and somewhat mediocre.

The "not so bad" situations become longer bad ones.

But what if you hit rock bottom?

What if your situation becomes so unbearable that you can't stand it anymore? What if your arguments with your partner spiral out of control? What if your boss engages in sexual harassment? What if you drown in debt?

You would take action.

You would take action to transform your life.

Today's agenda

- The region-beta paradox explained

- Solution #1: accelerate your bad-bad situation

- Solution #2: lower your critical threshold

The region-beta paradox

The region-beta paradox was coined by the American social psychologist Daniel Gilbert.

It describes this phenomenon where being worse off can be a blessing in disguise because it can ignite a fire within us to take action and address the problem head-on. On the other hand, when we are in that zone of mediocrity, we tend to get stuck in a state of stagnancy. We're caught in a comfortable yet unfulfilling limbo.

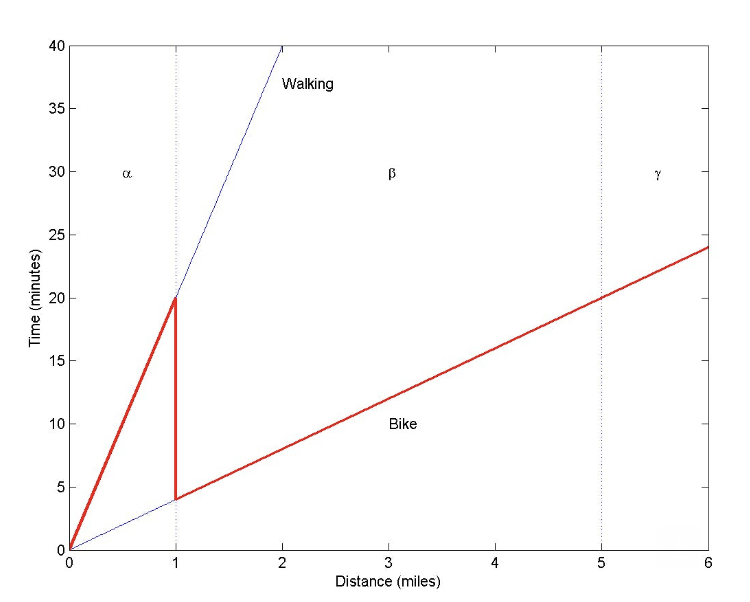

He supports his argument by using the following analogy: individuals decide to switch from walking to biking when reaching the critical threshold (here, it is 1 mile).

When the distance is less than 1 mile (= medium-bad situation), most people prefer to walk.

Anything beyond a mile (= bad-bad situation), they would choose biking.

Therefore, the paradoxical fact is within the region of up to 5 miles, biking gets you to your destination faster than walking a mile.

I personally don't think the graph illustrates the point perfectly.

The psychology meant is this mindset can be applied to various situations in daily life, such as staying in an okayish but unfulfilling financial situation.

Let me give you a money example.

Imagine you're the type who doesn't take care of your finances (blue line), living paycheck-to-paycheck with no savings, but no debt. It's not ideal, but you survive monthly. Your critical threshold is when you can no longer pay off your credit card. Then, you will do something about it (red line): you will start building your financial health, seek help, and get proper financial education.

The region-beta paradox applied to your financial health

That's why you often hear success stories from people who have gone through depression, homelessness, obesity, or abusive relationships—they hit rock bottom and found the motivation to change their circumstances.

But do you always have to sit and wait - for years sometimes - for this worst-case scenario to hit you square in the face?

The answer is no.

Here, I'm sharing 2 solutions.

Solution #1: accelerate your bad-bad situation (not recommended)

Not ideal, but if you must hit your lowest point to get moving, you might want to reach your bad-bad situation now!

For instance, if your mental threshold is maxing out your credit card to begin addressing your financial situation, or being unable to fully pay off your credit card debt, and you're already living paycheck-to-paycheck with zero savings, then perhaps it's worth considering.

Accelerate your bad-bad situation to reach your threshold faster!

[CAVEAT: I would not recommend this unless your threshold is very close from where you currently stand. For example, if your mental threshold is reaching $10K in debt, then go to solution #2]

Solution #2: move down your critical threshold (recommended)

How can you lower the threshold to your advantage?

Consider this: Instead of having a mental threshold about being indebted, what if your mental threshold became...

- ...Failing to save an extra $1,000 this month

- ...Feeling guilty about spending at least once a week .

- ..Experiencing daily stress related to money

Chances are, you’re more likely to take action now instead of waiting passively for the worst-scenario to come.

Lower your critical threshold so you can take action right now

instead of waiting

I'd suggest completing this threshold change with a writing exercise.

Take a few moments now to jot down all the potential impact according to 2 different scenarios:

Scenario #1, the cost of inaction: Continuing to live paycheck-to-paycheck, sporadically saving, without a concrete retirement plan, being anxious about money, and living your life by default.

Scenario #2, taking immediate action: elevating your financial questions and aspirations (shifting from “should I buy this?” to “what kind of wealthy life do I want?”), practice intentional spending and long-term investing to live your live by design.

What would you do? Who would you be with? Where would you be? Would you leave your job or start a side business? Would you break up with your partner or rebuild intimacy with them? Would you try that hobby you have always postponed? What if you win the lottery tomorrow? What will you do?

Be as precise as possible.

And most importantly, how would you feel? Would you feel confident, pretty, smart, courageous, peaceful, optimistic, reliable or respectful?

Interestingly, most of my clients wait until they start accumulating debts and find themselves unable to keep up with their credit card payments, that's when they finally give me a call.

I always tell them they have to be thankful for those debts, even though it was stressful back then, but that bad-bad situation made them take action and build the wealthy life they are right now.

At the end of the day, hitting rock bottom isn't too bad because it can be the catalyst for our greatest comebacks - but only if your rock bottom isn't too far off.

It's a powerful reminder that playing it safe may not always be the safest bet.

So, what is your breaking point?

Build your financial confidence to be in control of your critical threshold!

Sophie